POS health plan, or Point of Service plans, blend features of both HMO and PPO plans. They require members to choose a primary care physician (PCP). The PCP coordinates care and provides referrals to specialists. Members can see out-of-network providers but may pay higher costs. POS plans offer flexibility while encouraging managed care. Understanding these key aspects helps individuals select the right health plan for their needs.

How POS Health Plans Work: Key Features Explained

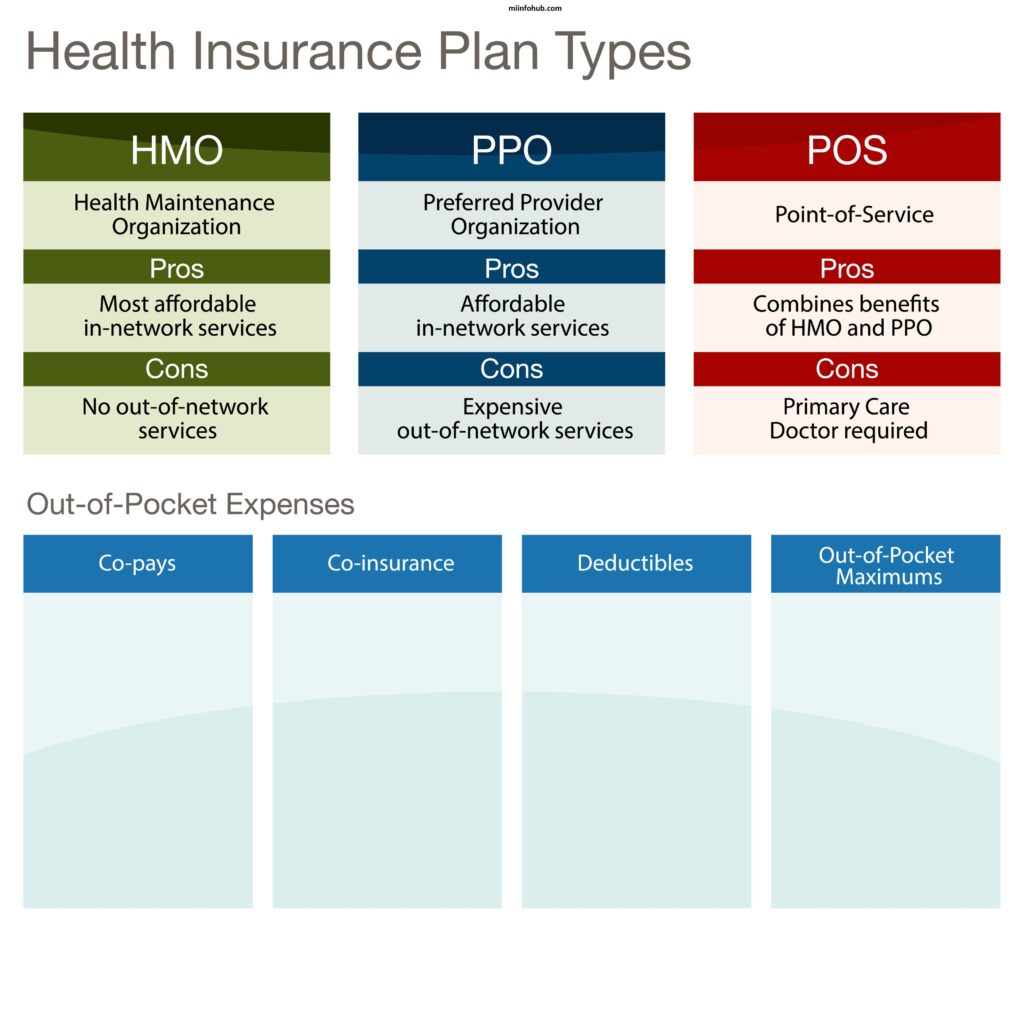

POS health plans operate by combining elements of Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). Here are the key features explained:

- Primary Care Physician (PCP): Members must select a PCP who serves as their main point of contact for healthcare. The PCP coordinates all care and provides referrals to specialists when necessary.

- Referrals: To see a specialist, members typically need a referral from their PCP. This helps ensure that care is well-coordinated.

- In-Network vs. Out-of-Network: POS plans have a network of preferred providers. Members save money by using in-network doctors and hospitals. They can see out-of-network providers, but at a higher out-of-pocket cost.

- Cost Sharing: Members usually pay a copayment for visits to their PCP and specialists. Deductibles may apply, especially for out-of-network services.

- Preventive Services: Many POS plans cover preventive services at no additional cost when provided by in-network providers. This includes routine check-ups and vaccinations.

- Flexibility: POS plans offer more flexibility compared to HMOs since members can access out-of-network care. However, doing so may involve higher costs.

- Claim Process: If members see out-of-network providers, they may need to file claims for reimbursement. This adds an extra step compared to in-network visits.

POS Health Plans vs. HMO And PPO: What Sets Them Apart?

| Feature | POS Health Plans | HMO | PPO |

|---|---|---|---|

| Primary Care Physician (PCP) | Requires a PCP for referrals | Requires a PCP for referrals | No PCP required |

| Network Flexibility | In-network preferred; out-of-network at higher cost | Limited to in-network providers | Can see any provider; higher cost for out-of-network |

| Cost Structure | Copayments and deductibles vary; costs depend on network usage | Lower premiums and out-of-pocket costs; in-network only | Higher premiums and out-of-pocket costs |

| Referrals | Requires referrals to see specialists | Requires referrals to see specialists | No referrals needed |

| Preventive Care | Often covers preventive services at no extra cost in-network | Emphasizes preventive care, often fully covered | May cover preventive services but with cost-sharing |

Benefits Of Choosing A POS Health Plan For Your Healthcare Needs

Choosing a POS (Point of Service) health plan offers several benefits for managing your healthcare needs effectively. Here are some key advantages:

- Flexibility: POS plans combine features of both HMO and PPO plans. You can choose to receive care from in-network providers for lower costs or go out-of-network for more flexibility, albeit at a higher cost.

- Primary Care Physician (PCP): With a POS plan, you select a PCP who coordinates your care. This relationship can enhance your healthcare experience and ensure that all your health needs are managed in a comprehensive way.

- Referral System: POS plans often require referrals to see specialists, promoting more organized care. This process ensures that you receive necessary consultations and follow-up care efficiently.

- Cost-Effective: By primarily using in-network providers, you can benefit from lower copayments and deductibles, making healthcare more affordable.

- Access to Specialists: While referrals are needed for specialists, having a PCP manage your care can streamline the process and ensure you see the right specialists when necessary.

- Preventive Care: Many POS plans emphasize preventive services, encouraging regular check-ups and screenings, which can lead to early detection and better health outcomes.

- Comprehensive Coverage: POS plans typically cover a wide range of services, including hospital stays, preventive care, and emergency services, ensuring you have access to essential healthcare.

Limitations What You Should Know

POS (Point of Service) health plans come with several limitations that you should be aware of when considering your healthcare options. Here are some key drawbacks:

- Referral Requirement: To see a specialist, you often need a referral from your primary care physician (PCP). This can delay access to specialized care and add an extra step to your healthcare process.

- Higher Costs for Out-of-Network Care: While POS plans offer flexibility in choosing providers, using out-of-network services typically incurs higher out-of-pocket costs. This can make care more expensive if you frequently see out-of-network specialists.

- Limited Provider Network: POS plans may have a smaller network of providers compared to PPO plans. If you have a preferred doctor outside the network, you might have to switch or pay more for their services.

- Complexity: The structure of POS plans can be confusing. Balancing in-network and out-of-network options, along with referral requirements, may complicate your healthcare decisions.

- Potential for Higher Copayments: If you choose to see out-of-network providers, you may face higher copayments and deductibles, which can strain your budget.

- Varied Coverage for Services: Not all services may be covered equally. Some plans might have specific limitations on certain types of care, leading to unexpected costs.

- PCP Dependency: Your healthcare experience largely depends on your PCP. If you don’t have a good relationship with your assigned physician, it could impact your overall satisfaction with the plan.

Cost Considerations: Are POS Health Plans Affordable?

When considering the affordability of POS (Point of Service) health plans, several factors come into play. These plans generally have lower premiums compared to PPO plans, making them appealing for budget-conscious individuals. However, out-of-pocket costs like deductibles, copayments, and coinsurance can add up, especially if you seek frequent care. While in-network services typically cost less, out-of-network care can lead to higher expenses. Some plans may also require referrals for specialists, which could incur additional fees. Overall, understanding these costs and comparing different plans is essential to determine if a POS health plan fits your budget. If you want to know more about what insurance does archwell health accept then click here.

How To Choose The Right Plan For You And Your Family

Choosing the right POS (Point of Service) health plan for you and your family requires careful consideration of several factors. Start by assessing your healthcare needs, including how often you visit doctors and if you have any ongoing medical conditions. Review the list of in-network providers to ensure your preferred doctors and specialists are included. Compare premiums, deductibles, and out-of-pocket costs to find a plan that fits your budget. Additionally, consider the flexibility of accessing out-of-network services, as this can impact your overall care experience. Finally, read the plan’s terms to understand referral requirements and covered services, ensuring the plan aligns with your family’s healthcare priorities.

Navigating The Network: In-Network vs. Out-Of-Network Providers In POS Plans

Navigating a POS (Point of Service) health plan requires understanding in-network and out-of-network providers. In-network providers have contracted rates with the insurance company, resulting in lower out-of-pocket costs. Patients must choose a primary care physician (PCP) from this network for referrals. Out-of-network providers do not have these agreements, leading to higher costs. While POS plans allow visits to out-of-network providers, using in-network services is generally more cost-effective, helping members make informed healthcare choices.

Frequently Asked Questions

What is a POS health plan?

- A POS (Point of Service) health plan combines features of HMO and PPO plans, allowing members to choose between in-network and out-of-network providers.

How do I choose a primary care physician (PCP)?

- Members must select a PCP from the plan’s network, who will coordinate their care and provide referrals for specialists.

Are referrals required for specialists?

- Yes, referrals from your PCP are typically required to see specialists within the network, but you can see out-of-network specialists without a referral, often at a higher cost.

What are the cost differences between in-network and out-of-network care?

- In-network care usually has lower copayments and deductibles compared to out-of-network care, which tends to be more expensive.

Can I visit any doctor or hospital?

- You can visit any doctor or hospital, but using in-network providers will save you money and ensure better coverage.

What are the advantages of a POS health plan?

- POS plans offer flexibility in choosing healthcare providers while also providing cost savings when using in-network services.

What limitations should I be aware of?

- Limitations include needing a referral for specialists and potentially higher costs for out-of-network care.

Are preventive services covered?

- Yes, most POS plans cover preventive services at no additional cost when using in-network providers.

How do I find in-network providers?

- You can find in-network providers through your insurance company’s website or by contacting customer service.

What should I do if I need care while traveling?

- If you’re traveling and need care, check if your plan covers out-of-network services and what the associated costs may be.

Real-World Examples: Success Stories

- Family Health Management

The Johnson family chose a POS health plan for its flexibility. Their primary care physician coordinated care for their two children, ensuring timely vaccinations and routine check-ups. When one child needed a specialist for a minor surgery, the referral process was seamless, and they saved significantly on out-of-pocket costs by choosing an in-network provider. - Chronic Condition Care

Maria, a 45-year-old with diabetes, opted for a POS plan that allowed her to see specialists without a long wait. Her PCP worked closely with an endocrinologist and nutritionist to develop a comprehensive care plan. This coordinated approach led to improved health outcomes and better management of her condition. - Emergency Situations

During a family vacation, the Smiths faced a medical emergency. Their POS health plan allowed them to access an out-of-network hospital, providing critical care without significant financial strain. Upon returning home, they found that many of the expenses were covered, thanks to the plan’s flexible structure. - Preventive Care Success

Tom, a 60-year-old, utilized his POS plan to prioritize preventive care. He regularly visited his in-network PCP for check-ups and screenings, which led to the early detection of high blood pressure. By managing his condition proactively, Tom avoided more severe health issues, ultimately saving on medical expenses. - Mental Health Support

Sarah struggled with anxiety and depression. Her POS health plan provided access to mental health professionals within the network. With her PCP’s referral, she started therapy sessions and received medication management, significantly improving her quality of life. - Childhood Asthma Management

The Parkers chose a POS plan that provided excellent coverage for their son’s asthma treatment. Their PCP connected them with an allergist and pulmonologist, facilitating a coordinated approach that included medication, education, and regular follow-ups. The family appreciated the low costs associated with in-network care. - Transitioning to a New Provider

After relocating, the Taylors needed to find a new PCP. Their POS plan allowed them to select a doctor in their new area easily. The transition was smooth, with the new provider quickly accessing their medical history and ensuring continuity of care. - Healthy Lifestyle Promotion

The Green family utilized their POS plan’s wellness programs, which included fitness classes and nutrition counseling. The plan’s coverage for preventive services encouraged them to adopt a healthier lifestyle, resulting in weight loss and improved overall health.